Top 10 Retirement Questions Railroaders Ask Before They Hang Up the Lantern or Put Away the Reverser

After decades of early mornings, brutal all-nighters, countless holidays away from home, 12+ hour days to keep America moving, retirement is finally in sight. But stepping off the rails into this new chapter brings a lot of questions—especially when you’re covered by the Railroad Retirement Board (RRB), not traditional Social Security.

Here are the 10 most common retirement questions railroaders ask—use with this railroader retirement guide to help you prepare with confidence, use with this railroader retirement guide

1. When am I eligible to receive Railroad Retirement benefits?

How Railroad Retirement Benefits Are Calculated

Railroad Retirement consists of two parts: Tier I and Tier II.

- Tier I is based on your combined railroad and Social Security-covered employment and calculated using Social Security formulas.

- Tier II is based solely on your railroad service and is calculated similarly to a private pension.

Tier I Formula (2025 estimates):

- 90% of the first $1,174 of average indexed monthly earnings (AIME)

- 32% of the AIME over $1,174 up to $7,078

- 15% of AIME over $7,078

Tier II Formula (2025):

- 0.007 (0.7%) x years of creditable railroad service x average monthly earnings (based on your top 60 months)

Example: If your high-60 average monthly earnings are $6,000 and you retire with 30 years of creditable railroad service:

- Tier II = 0.007 × 30 × $6,000 = $1,260/month

If you have 35 years instead of 30:

- Tier II = 0.007 × 35 × $6,000 = $1,470/month

Substantial Difference: That’s a $210/month increase, or $2,520 more per year, by working 5 additional years. Over a 20-year retirement, that’s $50,000+ in extra Tier II income—not counting COLA adjustments.

Most railroaders qualify for Tier I and Tier II benefits. If you’ve worked at least 10 years (or 5 years after 1995) in the railroad industry, you’re generally eligible for benefits starting as early as age 60 with 30 years of service.

Example: Joe worked 32 years as a locomotive engineer. He applied for full Railroad Retirement benefits at age 60 and started receiving monthly payments immediately.

Example: Mark worked 25 years in the railroad and decided to retire at age 62. Because he didn’t meet the 30-year service mark, he had to wait until age 62 to begin receiving reduced Railroad Retirement benefits.

2. What’s the difference between Tier I and Tier II benefits?

- Tier I is similar to Social Security and is based on your earnings.

- Tier II is more like a private pension—it reflects your railroad career and is an additional benefit.

Example: Maria’s Tier I benefit was calculated at $1,800/month. Because she spent 28 years in the railroad industry, she also received $900/month in Tier II benefits—for a total of $2,700/month.

3. Will my spouse receive any benefits?

Yes—if your spouse is at least age 62 or caring for your dependent child, they may qualify for a spousal annuity.

Example: Bob’s wife, Linda, turned 62 and applied for spousal benefits while Bob was receiving Railroad Retirement. She qualified for an additional $700/month based on Bob’s Tier I benefits.

4. How is Railroad Retirement different from Social Security?

Railroad Retirement typically provides higher benefits for career railroaders, thanks to the Tier II component. But the rules differ.

Example: Sam’s twin brother works in a non-railroad job and receives $2,000 from Social Security. Sam, with the same income history but 30 years in the railroad, receives $2,800 total between Tier I and Tier II.

5. What if I also worked outside the railroad?

The RRB and Social Security Administration coordinate benefits. If you have both types of earnings, they combine your credits but avoid paying duplicate benefits.

Example: Diana worked 12 years in the railroad, then 20 years in the private sector. Her Tier I benefit was adjusted to avoid double counting, and she received an additional Social Security component.

6. Do I need to enroll in Medicare when I turn 65?

Yes—but it depends on your current coverage.

- If you’re retired or don’t have employer coverage, enroll in Medicare Part A and Part B at 65.

- If you have creditable employer coverage, you can delay Part B.

✅ Tip: Confirm your current coverage is considered “creditable.”

Example: Tony retired at 62 and used his wife’s employer health plan. When he turned 65, he delayed Part B since her plan was creditable. He enrolled later penalty-free once her coverage ended.

7. Can I keep working after I retire and still get benefits?

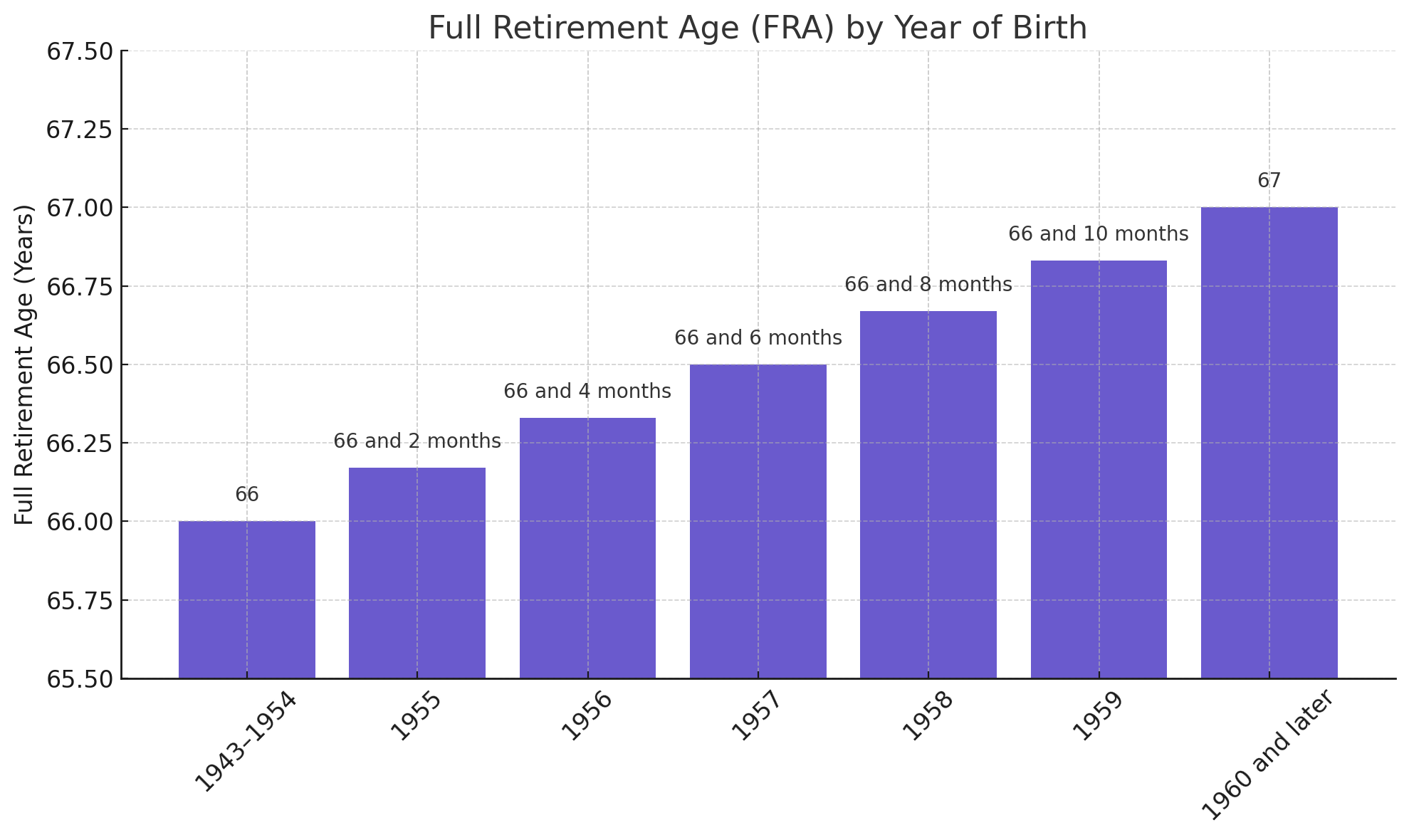

Yes—but there’s a catch if you’re under Full Retirement Age (FRA).

2025 Earnings Limits:

- Earn up to $22,320 with no penalty.

- Over that, the RRB deducts $1 for every $2 earned.

In the Year You Reach FRA:

- Higher limit of $59,520.

- $1 withheld for every $3 over the limit.

After FRA:

- No earnings limit. You keep all your benefits.

Example: Mike retired at 63 but took a part-time job making $30,000/year. He was $7,680 over the limit, so the RRB reduced his benefits by $3,840. Once he hit FRA at 67, the reduction stopped.

Tier II benefits are not reduced for working after retirement.

8. What happens if I become disabled before retirement age?

The RRB offers occupational disability benefits for those unable to perform their railroad job.

Example: Frank had 22 years of service when a back injury ended his rail career at 58. He qualified for occupational disability benefits that paid him monthly until he transitioned to full retirement benefits at age 60.

9. How do I estimate what my monthly retirement check will be?

You can:

- Contact the RRB for an official estimate

- Create a myRRB account online

Example: Jill logged into myRRB and saw her projected benefits at age 60, 62, and 67. This helped her decide to retire at 62 with enough savings to supplement her monthly checks.

10. What kind of insurance do I need after retirement?

If you are Medicare eligible:

2025 Medicare Part B Premiums & Deductibles

| Income (MAGI) | Total Monthly Part B Premium |

| ≤ $106,000 (individual) or ≤ $212,000 (joint) | $185.00 |

| $106,001–$133,000 / $212,001–$266,000 | $259.00 |

| $133,001–$167,000 / $266,001–$334,000 | $370.00 |

| $167,001–$200,000 / $334,001–$400,000 | $480.90 |

| $200,001–$500,000 / $400,001–$750,000 | $591.90 |

| ≥ $500,001 / ≥ $750,001 | $628.90 |

- Standard deductible: $257/year

- Based on income from your 2023 tax return

Once employer coverage ends:

- Sign up for Medicare

- Consider Medigap or Medicare Advantage

- Explore Part D, final expense, and long-term care coverage

For a Railroader Retiring at Age 60 and Not Yet Eligible for Medicare

Another area this railroader retirement guide discusses is healthcare before Medicare. There are several health insurance options to bridge the gap until age 65:

1. Union-Provided Health Plans (if applicable):

- GA-46000 Plan: This is a comprehensive health insurance plan provided to eligible railroad retirees and their dependents. To qualify, you must have at least 30 years (360 months) of railroad service and retire at age 60 or later. The plan covers hospitalization, surgical procedures, physician visits, and other essential medical needs. It is provided at no cost to eligible retirees and continues until age 65, when Medicare becomes primary.

- GA-23111 Plan E: This plan acts as a supplement to GA-46000, providing additional benefits such as outpatient care and coverage for services not fully paid by GA-46000. The plan is optional and must be purchased separately. As of 2025, the monthly premium is approximately $350 per person.

- Railroad Employees National Health and Welfare Plan (formerly GA-23000): This plan may provide continued limited medical benefits for some railroad retirees who do not qualify for GA-46000. Eligibility requirements are stricter and based on employment classification, years of service, and labor agreements. Coverage under this plan typically includes basic medical and hospital services, but may require higher out-of-pocket costs than GA-46000.

- GA-46000 and GA-23111 Plan E: If you have at least 360 months (30 years) of service and retire at age 60 or later, you and your dependents may be eligible.

- GA-46000: Free coverage for you and your dependents until age 65.

- Plan E: Supplemental plan available for purchase. The current cost for GA-23111 Plan E is approximately $350/month per person. If you’re covering both yourself and your spouse, you would need to purchase two separate plans, totaling around $700/month.

- Railroad Employees National Health and Welfare Plan (formerly GA-23000): Offers limited medical benefits to qualifying retirees ages 60–65.

- Other Union Plans: Check with your union for plan specifics in your labor contract.

2. COBRA:

- Extends your employer coverage for up to 18 months (or longer in some cases).

- ⚠️ You pay the full premium + 2% admin fee — can be expensive.

- Estimated cost: COBRA premiums for railroaders can range between $800–$1,200/month per person depending on your prior employer plan. For a couple, that could be $1,600–$2,400/month.

3. Health Insurance Marketplace (Affordable Care Act):

- Purchase through the exchange.

- No denial for pre-existing conditions.

- Premium tax credits and subsidies may be available.

- Enroll during Open Enrollment (Nov 1 – Jan 15) or after losing coverage.

- Estimated cost: A Silver-level ACA plan for a 60-year-old in Kansas could range from $600–$800/month before subsidies. With tax credits based on income, this can drop to under $200/month in some cases.

4. Private Insurance:

- Buy direct from an insurance carrier.

- ⚠️ Not eligible for government subsidies.

5. Spouse’s Plan:

- If your spouse has job-based coverage, you may qualify as a dependent.

6. Medicaid (if eligible):

- Based on income or disability.

- Check your state’s requirements.

Key Considerations:

- Cost: Premiums, deductibles, and out-of-pocket expenses vary.

- Coverage: Choose a plan that fits your needs.

- Eligibility: Each plan has specific rules.

- Timing: Avoid lapses in coverage by planning ahead.

Example: Jeff retired from the railroad at 60 with 33 years of service. He and his spouse were covered under GA-46000 until they turned 65 and enrolled in Medicare. Jeff also added Plan E for extra peace of mind.

This is where I come in. I’ve been in the cab for over 30 years myself—I get what you’re going through, that’s why I put together this railroader retirement guide. Let’s find a solution that fits your future.

Bonus: Other Key Information Railroaders Should Know

The “60/30 Rule” Explained

To receive full retirement benefits at age 60, you must have 30 years (360 months) of creditable railroad service. Falling short by even a few months can significantly impact your benefits.

Example: Ed has 29 years and 10 months. If he retires at 60, he won’t qualify for full benefits. By working just two more months, he becomes eligible under the 60/30 rule, significantly increasing his payout.

Cost-of-Living Adjustments (COLAs)

- Tier I COLA is based on the Consumer Price Index (CPI), like Social Security.

- Tier II COLA is typically lower and based on a different formula.

Example: In 2024, Tier I rose by 3.2%, and Tier II rose by 0.6%. A retiree with $2,800/month total saw an increase of about $75/month overall.

Survivor Benefits

Railroad Retirement offers benefits to surviving spouses and dependents.

- Tier I Survivor Benefits: These are similar to Social Security survivor benefits. The surviving spouse can receive up to 100% of the employee’s Tier I amount, depending on age, other income, and eligibility. Benefits may be reduced if the surviving spouse is under full retirement age or receiving other government benefits.

- Tier II Survivor Benefits: The surviving spouse can receive up to 50% of the deceased employee’s Tier II benefits. These are calculated based on the railroader’s years of service and highest-earning years. Unlike Tier I, Tier II survivor benefits are not offset by Social Security.

- Children’s Benefits: Dependent children may qualify for benefits until age 18 (or 19 if still in high school). Disabled adult children may be eligible for benefits as long as the disability began before age 22.

Example: When retired railroader Steve passed, his wife continued receiving 100% of his Tier I and 50% of his Tier II benefit, which provided essential income support.

Survivor Benefits Comparison Chart

| Benefit Type | Max % Payable to Spouse | Taxable Status | Offset by Social Security |

| Tier I Survivor | Up to 100% | Partially Taxed | Yes |

| Tier II Survivor | Up to 50% | Fully Taxed | No |

- Tier I Survivor Benefits: These are similar to Social Security survivor benefits. The surviving spouse can receive up to 100% of the employee’s Tier I amount, depending on age, other income, and eligibility. Benefits may be reduced if the surviving spouse is under full retirement age or receiving other government benefits.

- Tier II Survivor Benefits: The surviving spouse can receive up to 50% of the deceased employee’s Tier II benefits. These are calculated based on the railroader’s years of service and highest-earning years. Unlike Tier I, Tier II survivor benefits are not offset by Social Security.

- Children’s Benefits: Dependent children may qualify for benefits until age 18 (or 19 if still in high school). Disabled adult children may be eligible for benefits as long as the disability began before age 22.

Example: When retired railroader Steve passed, his wife continued receiving 100% of his Tier I and 50% of his Tier II benefit, which provided essential income support.

Taxation of Benefits

- Tier I is taxed like Social Security—partially based on your income.

- Tier II is fully taxable like a private pension.

✅ Tip: You can set up automatic withholding to avoid surprises come tax time.

How to Apply for Railroad Retirement

- Contact your nearest RRB office 3 months before retirement.

- Documents needed: proof of age, marriage certificate (if applicable), Social Security card.

- You can also schedule a pre-retirement consultation with the RRB to get personalized help.

Final Tip

Retirement from the railroad isn’t just about quitting a job—it’s about entering a new phase with clarity, security, and a plan. Whether you’re 6 months out or 6 years away, it’s never too early to prepare and I hope this railroader retirement guide helped. Contact Us at TCG Insurance Solutions for any questions you may have. Call Paul at 913-390-3220

Did I mention I am a railroader too? I have 32 years in and know you have many questions, I hope this railroader retirement guide helps!

That is me in 2010, standing, ready to pilot the UP3985 Steam Passenger Special from KC to Marysville.

If you would like a PDF version of this guide, Please use the form below so I can get it mailed to you